Can your firm’s management reporting support your leaders and managers during pandemic high-pressure and its economic fallout… and into the accelerating future of professional services?

An article by Sebastian Hartmann and Stephan Kaufmann

Across the world and in most economies and industries, we are not only fighting a pandemic and facing a recession but also see the pace of change accelerating. Consulting, legal, tax, outsourcing, and technology services firms are traditionally riding this wave of change and shape therewith arising client challenges and responses. Only this time, they are right in the middle of it – and need to transform themselves.

Being under pressure for quite some time, the traditional time & material model for professional services continues to erode with remote working and virtual engagement models on the rise. Personal relationships, high billable daily or hourly rates, and great utilization alone are no longer a recipe for success. Technology is moving to the center of attention, and firms are spending more and more – absolutely but also relative to their revenue. If solely treated as a cost position, it becomes a race to the bottom. Instead, if considered a revenue driver, technology paves the way for new business models. The whole architecture and value chain of services is, therefore, evolving towards a new reality for the professions. “Smart people” are not the “product.” Maximizing individual partner income is not enough motivation. Neither to drive significant scale nor to justify adequate technology investments. So, the management playbook has changed – across consulting, legal, tax, accounting, and other professional services firms (PSFs). But how can firm leaders manage their new reality based on facts and figures? What does a future-ready management reporting look like in professional services?

Quite often, we find that while both the value and cost management levers have changed, many finance and controlling departments are still producing the same old reports, if any. Their focus often remains on net sales, charge-out rates, utilization, and realization. But it is increasingly questionable whether the traditional KPI sets suffice to manage a professional services business – especially if this business is leveraging technology, virtual client collaboration models, digital sales channels, shared delivery centers, suppliers, a contingent workforce, freelance expertise, alliance partners and co-creating new solutions with a growing ecosystem of players around clients.

The next generation of management reporting needs to combine different perspectives and new dimensions to create a more meaningful picture and provide actionable transparency to leaders and managers in professional services:

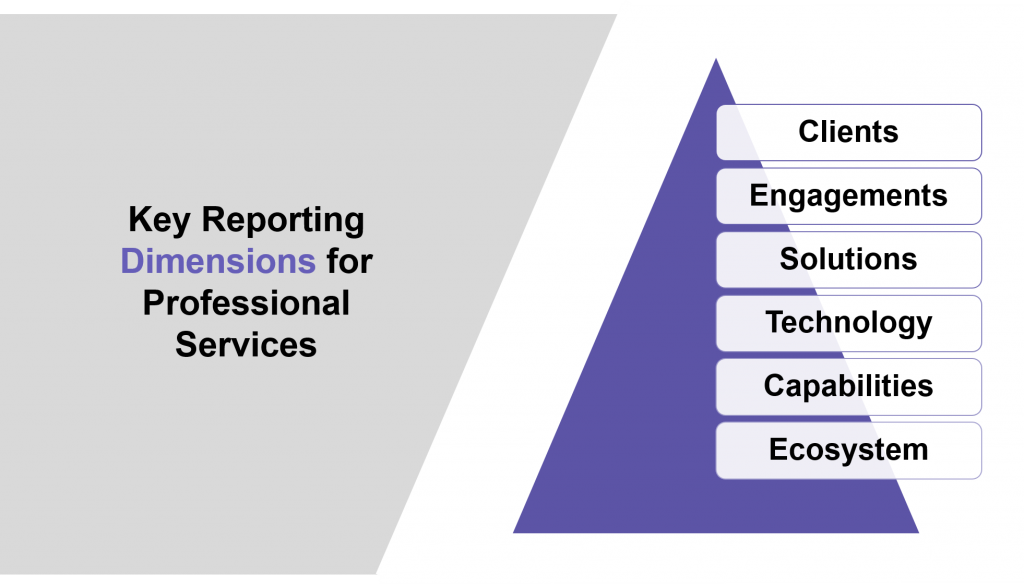

- Clients: “Client reporting” is typically one of the more mature reporting dimensions, where most PSFs have a reasonably good understanding of how much revenue is achieved per client or account and whether account revenues are growing or declining. Nonetheless, many PSFs already stumble when asked about single client profitability and penetration of services. They have great difficulties to run reports regarding their share of wallet with a particular client or struggle to segment their client base beyond an industry classification, e.g., based on business models, relationship strengths or compositions, CxO addressees, credit scores, risk exposures, and other attributes. Being able to determine the state of your client base in times of crisis is a painful lesson, which many PSFs are learning at this very moment. Another increasingly important reporting angle evolves around the actual client experience. With a massive shift towards more virtual collaboration or even completely digital delivery models, this perspective may become one of the key advantages for firms capable of providing superior and integrated digital and personal relationships, interactions, service deliveries, and client journeys. So, being able to analyze your client experiences holistically is an essential reporting capability for PSFs going forward.

- Engagements: We see vast differences in the way engagements (or projects, cases, matters, etc.) are treated in reporting. Many firms simply leave it to the responsible partner to keep engagements on track and clients happy. In other words, they provide no assistance or systematic management approaches. Overall, only a surprisingly small percentage of PSFs can report on anything more elaborate than count, size, volume, and resourcing of engagements. Indicators of operational delivery performance or even client success rarely make it beyond the team itself. Even fewer firms truly aggregate and include operational performance reports within their management and leadership reporting. Furthermore, as PSFs shift toward subscription-based, XaaS, or managed service business models and consequently more digital value chains, the nature of engagements is also changing significantly – requiring new angles to engagement reporting, such as incorporating phases or lifecycle information, insights on service levels, or usage and consumption patterns. We urge firms to adjust their definitions of what client engagements look like, how they evolve – and how they should be managed and reported.

- Solutions: As firms begin to re-architect their value chains and become more professional in the way technology, data, new capabilities and resources are leveraged, a reporting dimension is taking shape where all of this comes together: „Solutions“ – the term for services, products, and their combinations. In other words, this is about “what” is truly being delivered to clients – and how solutions (services, products) are performing across multiple clients, engagements, offices, and teams. Almost every industry or company would be quick to confirm the importance of this reporting dimension. Meanwhile, most PSFs still have severe deficits when it comes to understanding and reporting around their ill-defined services and/or products. This leaves the management clueless or reliant on gut feeling when it comes to related investment decisions, strategic analyses, or even the identification of operational solution and delivery management levers and potential. Solution-centered reporting for PSFs should be made granular enough to have meaningful conversations about the work being delivered. We recommend including at least essential aspects such as revenues and profitability (across clients, engagements, etc.), budget deviations, operational performance, and ROI/NPV indicators.

- Capabilities: Capability groups (often called practice groups, service lines, etc.) are traditionally one of the more mature reporting dimensions in PSFs. They are typically managed based on their people structure, utilization, and some information on the group’s involvement in client work. The resource and utilization numbers of capability groups are often used as the foundation for annual sales planning processes – which unfortunately neglects market potential and a growth-oriented sales view. The limits of the management reporting for capability groups are typically reached when it comes to skill profiles, learning and development paths, or strategic analyses through a client and solution portfolio lens. As professional services evolve, this reporting dimension needs to shape a matrix view with clients and solutions.

- Technology: The more solutions or services are underpinned by technology, the more it is critical to gain actionable transparency about the associated costs and consumption patterns – especially when clients are to be billed. The reality for most PSFs, however, is one far away from charging technology to their clients. Managing technology can be a daunting challenge in itself. And so is transforming an information & technology department (I&T) from an internal “behind the scenes” infrastructure provider or service desk to a value engine within the firm. I&T should not only understand the primary business on a much more operational level but also become an accepted partner thereof. One essential cornerstone of this transformation is creating the reporting capability to distribute I&T costs across engagements through “I&T services.” To do so, the I&T organization must develop a service portfolio that can be comprehended (business jargon) and consumed (price and unit measure) by the business. Thereby, the business is enabled to consider technology costs in its client proposals and ensure accurate billing to clients on a consumption basis. Typically, the I&T organization benefits from developing three stakeholder-specific views. One for finance, one for I&T, and one for the business. Each view with a distinct lingo to address the respective stakeholders in a meaningful way. The business view, we find, often poses challenges to I&T organizations whereas both finance as well as I&T views are typically available. The business view, in contrast, does require a sound understanding of the business and its solution portfolio.

- Ecosystem: Across professional services, we find a growing awareness of ecosystems – most notably through the ever-increasing number and intensity of collaborations between different firms, technology partners, alliances, suppliers, or even individual freelance experts. The integration of those ecosystem connections and players as well as the interactions, transactions in the management reporting is, however, an underdeveloped perspective (at best). Even simple spend analytics are a challenge for many firms, which have understaffed and immature procurement functions. With growing spend levels and dependence on other parties for their market success, this lack of reporting quality can not only be costly but also negatively impact the topline for PSFs. It is difficult, for example, to align joint sales activities without shared pipeline views between the involved parties. Jointly delivering with suppliers can also turn into a nightmare when there is no aligned understanding of the financial implications for both provider sides – and how they tie into success for clients.

Gavin Gray, COO of K&L Gates, echoes our reporting dimensions picture and the underlying paradigm shift: “We are moving from lawyers practicing law towards delivering legal solutions – and managing not just a legal, but a professional services business. We are moving our mindset around firm administration and management from a necessary housekeeping “overhead” burden to a differentiating capability that is more directly relevant to the exceptional delivery of client service. Management reporting, which allows us to better serve our clients – not just in hindsight, but “live” and continuously – is a key pillar for us. Client insights, solution and service performance, our use of technology and capabilities as well as our ecosystem activities are the essential ingredients for a more relevant and dynamic infrastructure that is capable of supporting our firm strategy and execution.”

To elevate a firm’s reporting maturity, it is critical to establish a sound understanding of the firm’s strategic ambition – which in turn shapes the reports within and across all management dimensions. A mature and impactful management reporting, however, needs more than just the right strategy and ticking of content boxes.

Management reporting should first and foremost serve the needs of the people in charge of managing the firm. In a professional services context, this may well include a considerable percentage of all employees – on potentially all hierarchy levels. To provide value, reports need to be pre-designed for specific roles and allow for customization driven by individual information needs. Mature firms use reporting to trigger actions automatically and thereby steer behavior. This goes beyond plain report design but includes the related communication processes and domain management mechanisms. Report addressees should find it easy to derive appropriate actions from reports and understand their personal or role-specific contribution to better firm performance. The organizational setup of the reporting function is another pillar, which needs careful design – and is highly dependent on the firm’s management structure, culture, and the reporting maturity (e.g., in terms of robustness or automation). Many reporting functions only serve as report producers and distributors with little involvement in the adjacent management processes and discussions. This setup often creates a disconnect on the data and content levels, too, which lowers the value of the reports or even creates “alternative truths.” Management reporting needs to evolve towards an institutionalized capability of the firm – a capability that is just as essential to serving clients, as the professionals themselves, the data and knowledge they bring to the table, or the technology deployed. As such, reporting functions need to foster a data-driven culture within the firm – and work hand in hand with I&T teams to deploy appropriate, user-friendly reporting tools for leaders, managers, professionals, and support staff or any other role and function within the firm. Ease of use for actionable management reporting is, however, not a tool selection question. It is much more about the integration of relevant reporting information within the right management information systems in processes, workflows, and collaboration spaces. In short: The information needs to be available wherever it is needed or useful. Ultimately, mature reporting organizations must be deeply embedded in the business management approach, driven by business-value and leverage technology to automate, accelerate, and continuously enhance reporting.

So, in the light of the pandemic, an economic downturn, and an unparalleled technological upheaval across professional services, we urge firm leaders to take a careful look at their management reporting – and to invest in its maturity and future-readiness. It is, after all, one of the most essential tools for any leadership and management role.